Mar 1, 2026

Why the nexts trillion dollars in onchain credit demands a fundamentally different architecture.

There’s a narrative in DeFi that lending pools are good enough. That variable rates, shared risk, and utilization curves are the natural architecture for onchain credit. That anyone building something different is chasing theoretical elegance at the expense of practicality.

I understand the logic. Pools were the right architecture for DeFi’s first chapter. Liquidity was thin. Markets were immature. L2s were unavailable. Building what was technically feasible onchain was the correct call. But somewhere along the way, we started confusing “what we could build” with “what credit markets actually need.”

DeFi built what was technically feasible onchain, not the architecture credit markets would design from first principles. We’ve been rationalizing it as optimal ever since.

The Myth of Revealed Preference

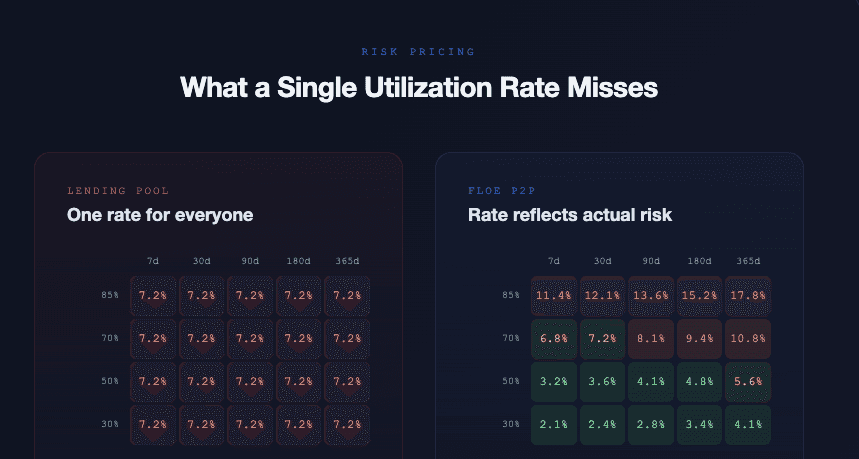

Look at onchain borrowing data and you’ll see most activity clustered at 77–86% LTV. The easy conclusion: borrowers want max leverage, and conservative lending is a niche nobody cares about.

That conclusion is wrong. It confuses behavior shaped by architecture with actual preference.

In a shared lending pool, a conservative lender at 50% LTV earns the exact same utilization-curve rate as someone at 85% LTV. Risk is socialized, but pricing isn’t differentiated. There’s no economic reward for being prudent. Of course participants push to the edge—the system literally incentivizes it.

That’s not revealed preference. That’s a rational response to an architecture that doesn’t compensate risk granularity.

Change the architecture and you change the behavior. When you can actually price a 50% LTV loan differently than a 75% one or under collateralized—with different rates reflecting different risk or product lines or underwriters or lenders—the conservative option becomes economically viable. It hasn’t been rejected by the market. It’s never been properly offered.

The conservative option hasn't been rejected. It just hasn't been properly compensated.

The Pooled Architecture Was a Constraint, Not a Choice

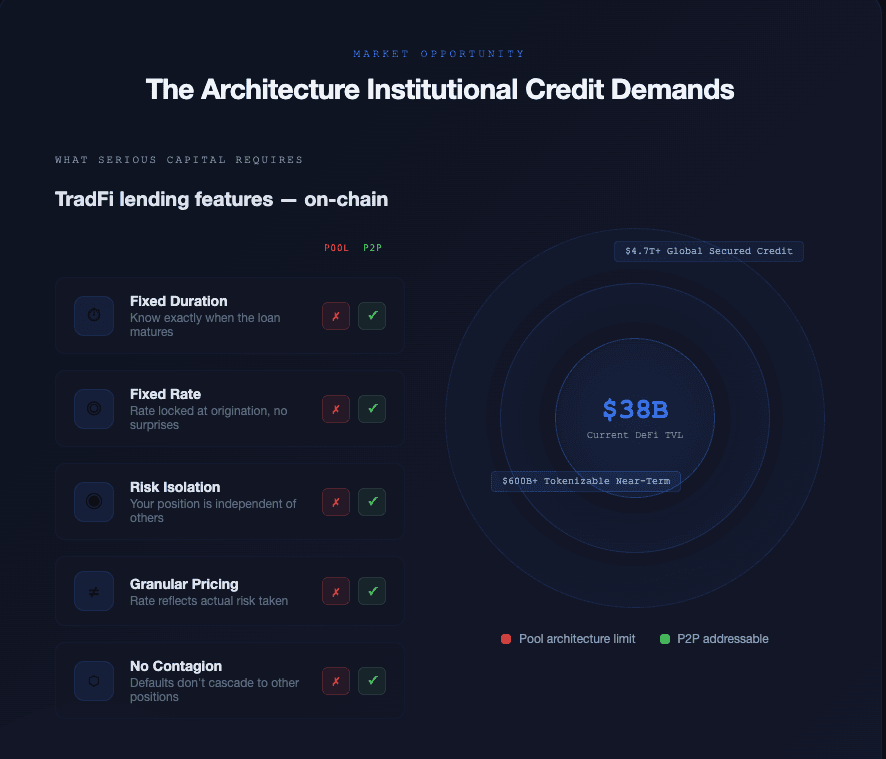

Early DeFi optimized for immediate liquidity because markets were thin. Pooled, variable-rate structures dominated because they were the simplest thing that could work on-chain with the infrastructure available. But it’s worth noting something striking: these structures are almost nonexistent in traditional secured credit markets.

In TradFi, risk-adjusted, fixed-term lending with maturities and repayment terms is the default for any serious scale. Fixed duration. Individualized pricing. Isolated risk. That’s not some theoretical ideal—it’s how a $4+ trillion market actually operates, because borrowers and lenders deploying real capital demand certainty.

The fact that DeFi looks nothing like this doesn’t tell us borrowers and investors / lenders prefer pools. It tells us pools were what the technology allowed. As infrastructure matures, pricing precision and term structure tend to follow. We’re watching that evolution happen in real time—protocols across the space are moving toward fixed rates, isolated markets, and curator-driven risk engines. The direction is clear.

The Perps Analogy Doesn’t Apply to Credit

There’s an argument that perpetual swaps beating expiring futures proves DeFi users reject structure in favor of frictionless leverage. It’s a compelling analogy—for speculation. It tells you almost nothing about credit.

Secured lending isn’t speculation. A 30-day loan at 60% LTV against tokenized T-bills is fundamentally different from a leveraged long on ETH. Different lender. Different borrower. Different risk profile. Different expectations around duration, certainty, and counterparty exposure.

Applying perp-market logic to credit infrastructure is like concluding that because most retail investors use commission-free trading apps, institutional prime brokerage is unnecessary. They’re different markets serving different participants with different requirements.

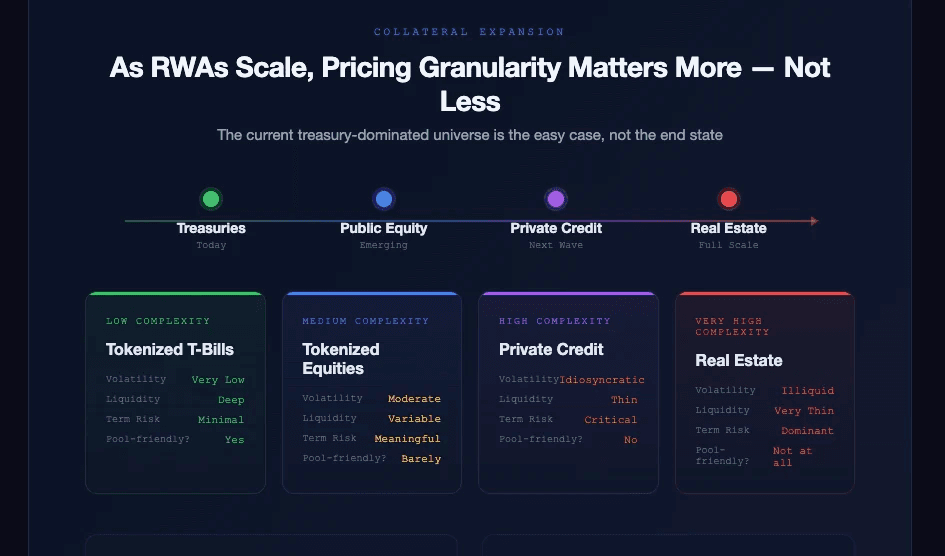

RWAs Make Granular Pricing More Important, Not Less

There’s an intuitive argument that lower-volatility RWA collateral flattens the risk surface, making per-loan pricing irrelevant. If both a 30% and 70% LTV borrower are safe against tokenized treasuries, why differentiate?

That’s the easy case. It’s not the end state.

Granular pricing isn’t just about collateral volatility spreads. It’s about term risk, counterparty risk, and structural risk. A 30-day loan at 60% LTV against tokenized T-bills is a completely different product than 180 days at 70% against the same asset. Pools can’t differentiate those two loans. A peer-to-peer architecture can.

And as RWA collateral expands beyond treasuries into tokenized equity, private credit, and real estate, the volatility profiles diverge dramatically. The current low-vol, treasury-dominated universe is the starting condition, not the permanent one.

Today’s low-vol RWA universe is the easy case, not the end state.

The $4 Trillion Question

Traditional secured credit (where terms are fixed, risk is isolated, and pricing reflects individual loan characteristics) isn’t a niche. It’s the backbone of global finance. It exists at that scale because institutional participants won’t deploy capital without the features pooled architecture can’t provide: duration certainty, individualized pricing, and structural isolation.

As tokenized assets scale, so does the addressable market for onchain credit with those characteristics. The “build for the borrower who actually shows up” framing assumes today’s DeFi borrower is the permanent DeFi borrower. That’s a bet against the entire RWA thesis.

The next wave of onchain credit participants—institutions, RWA originators, credit professionals, structured product desks—expect the infrastructure that traditional finance provides. They won’t accept shared pools with variable rates any more than a pension fund would accept a utilization-curve rate on a $50 million facility.

What We’re Building at Floe

Floe is the first peer-to-peer structured credit protocol. Direct borrower-lender matching with fixed terms, maturities, repayment terms. No shared pools. No socialized losses. No variable rates that change while you sleep.

We’re live on Base. We’re not chasing the last 20% of theoretical efficiency from isolated pools. We’re building the architecture that the next $4 trillion in onchain credit actually requires from the ground up, with the borrower and lender experience that scales beyond crypto-native leverage.

The question isn’t whether pools worked. It’s whether they’re the endpoint, or just the starting point.