Mar 8, 2026

The first rigorous game-theoretic analysis of intent-based markets — Chitra, Kulkarni, Pai & Diamandis (2024) — reaches a counterintuitive conclusion: restricting solver entry can make users better off.

We built Floe's solver architecture around that finding. Here's what the paper gets right, where it doesn't apply to lending, and why both conclusions point the same direction.

What the Paper Says

The setup: users post intents, solvers pay entry costs, compete in an auction to fill them. The core result is that equilibrium participation is asymptotically negligible: O(√n) solvers enter from a pool of n potential participants. With 100 potential solvers, roughly 5–10 actually show up.

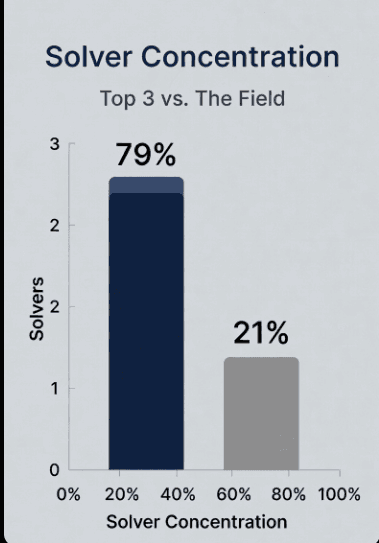

UniswapX confirms this empirically: 2,000+ historical filler addresses, 12 active in January 2024, top 3 handling ~79% of volume.

The deeper finding: when solver effort is congestive, ie each additional solver degrading everyone else's effectiveness without improving user outcomes, a welfare-maximizing planner should restrict entry further. The paper's framing: "a planner who aims to maximize user welfare may actually prefer to restrict entry, resulting in limited oligopoly." Fewer solvers face less congestion, invest more in each match, and users come out ahead.

Where It Maps to Lending, And Where It Doesn't

The paper models swap markets, where solver effort drives price discovery. More solvers searching more liquidity sources produces better prices. That's the benefit side of the tradeoff.

Lending removes that benefit entirely.

In Floe, interest rates and other credit terms are pre-specified by both parties. LTV is pre-specified. Collateral pricing comes from Chainlink/Pyth, not solver search. The solver's job is deterministic compatibility matching: check rate overlap, LTV gap, duration, repayment terms, amount availability. There's no price to discover.

That means: the congestion costs (duplicate execution, reverted transactions, wasted gas) stay exactly as the paper models. The competition benefit (better outcomes through solver effort) goes to zero. The case for a curated solver set is stronger in lending than anything the paper's swap-market analysis produces.

Two Architectural Properties the Paper Doesn't Model

Offchain intents create a second reason to gate access. Floe's offchain intents live in a private indexer and are never broadcast to the mempool until match execution. A closed solver set preserves this. Open access means opening the indexer, which reintroduces the MEV surface the offchain design eliminates. There's a cost to openness beyond congestion.

Borrower-set commission neutralizes the oligopoly concern. The paper's worry with restricted entry is solver rent extraction. In Floe, matcherCommissionBps is signed by the borrower at intent creation — a monopolist earns exactly what a competitive solver would. Restricting entry doesn't move fees. The one downside of a curated set simply doesn't apply here.

What We Built and Where We're Headed

Today: closed, team-operated solvers. They handle matching efficiently, MEV protection is intact, and fees are borrower-controlled. The real gap is redundancy: a single solver going down means no matches.

Next: a small allowlisted set of 2–5 independent operators. Not open competition but a deliberate, gated expansion. Indexer access stays restricted. Solvers take on uptime SLAs and have reputation at stake. Market partitioning minimizes gas races. The theoretical optimum the paper describes, implemented with the specific mechanics lending requires.

Fully open is not on the roadmap. Theory and architecture both argue against it.

The Short Version

The research says open solver competition naturally concentrates, and under the right conditions restricted entry is welfare-optimal. Lending removes the one condition where open competition helps. Our offchain architecture creates an additional reason to gate access. And our commission structure eliminates the rent-extraction risk that makes restricted entry feel uncomfortable.

We're not avoiding openness because we can't build it. We're avoiding it because every lens from game theory to MEV protection to protocol mechanics points the same way.

Chitra, T., Kulkarni, K., Pai, M., & Diamandis, T. (2024). "An Analysis of Intent-Based Markets." arXiv:2403.02525.